The Silent Advisor in the Room

A landmark new audit from Haute Wealth reveals that America’s most-used AI engines are giving ultra-high-net-worth families dangerously wrong estate planning advice—and the consequences may be irreversible.

For decades, the wealthiest American families have made their most consequential financial decisions in the company of a small, trusted circle: estate attorneys, fiduciary advisors, family office principals, and specialist insurance professionals whose entire careers are built around getting these calls right.

That circle now has an uninvited guest. Quietly and almost universally, AI engines have inserted themselves into the earliest stages of ultra-high-net-worth planning—answering questions, framing options, and shaping the terms of debate before a single human professional enters the room. A new joint study from Haute Wealth, the wealth-planning vertical of Haute Media Group, and 5W, the AI communications firm, now puts a name to what has long been suspected: those engines are getting it dangerously wrong.

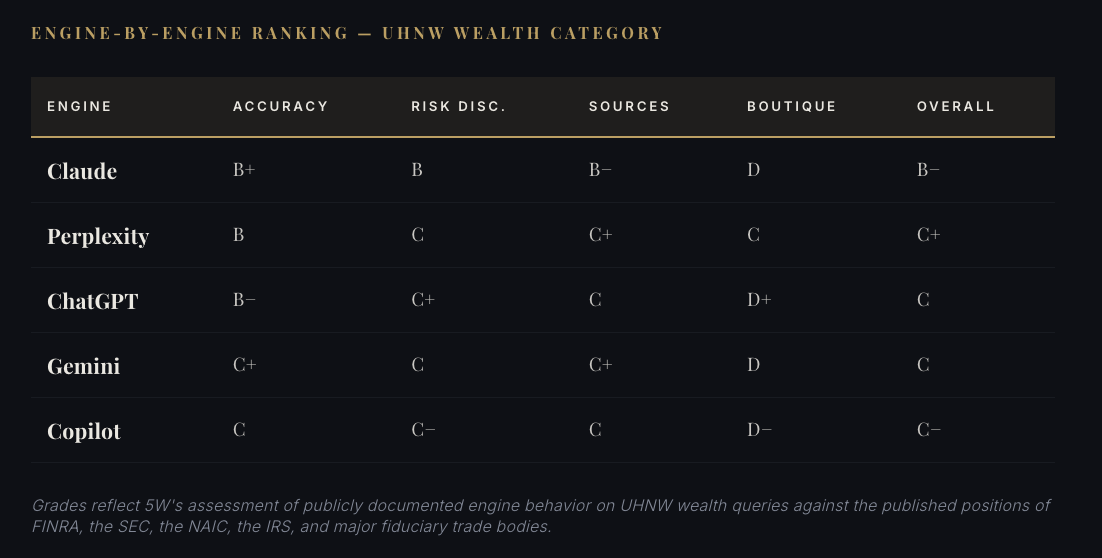

The Wealth AI Audit reviewed how ChatGPT, Perplexity, Gemini, Claude, and Microsoft Copilot respond to UHNW queries across six high-stakes categories: premium financing, private placement life insurance, irrevocable life insurance trusts, estate liquidity, business succession, and charitable legacy planning. What the researchers found should concern every family principal, fiduciary, and regulator paying attention.

|

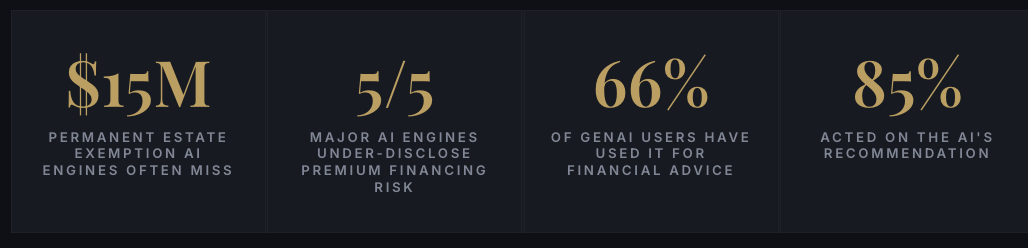

$15M New federal estate exemption per person as of Jan 1, 2026 |

5 Leading AI engines audited across 6 UHNW planning categories |

$30M Exemption for married couples — still cited incorrectly by AI |

The Tax Advice That No Longer Exists

The audit’s most alarming finding concerns a piece of federal tax law that was quietly retired nearly a year ago. For years, estate planners operated under the shadow of a looming “sunset”—a provision of the 2017 Tax Cuts and Jobs Act that would have slashed the federal estate, gift, and generation-skipping transfer exemption from roughly $13 million per person back down to approximately $7 million when the law expired.

That sunset is gone. President Trump signed the One Big Beautiful Bill Act into law on July 4, 2025, permanently raising the federal exemption to $15 million per person—$30 million per married couple—effective January 1, 2026, indexed for inflation thereafter. It was one of the most consequential estate planning developments in a generation.

Every AI engine audited is still advising clients as though the sunset is live.

The reason is structural. AI training data is saturated with pre-OBBBA advisor content—years of articles, guides, and planning memos written in anticipation of the sunset. Those engines are drawing on that history and surfacing it as current advice. A principal who asks an AI whether she should accelerate gifting to “lock in” the higher exemption before it expires may receive a confident, detailed, and wholly obsolete answer—and may act on it irrevocably before a human professional corrects the record.

“AI is now the silent advisor in the room when ultra-high-net-worth families make their most important decisions. That is a risk no fiduciary, no family principal, and no regulator can ignore.”

— Kamal Hotchandani, Founder & CEO, Haute Media Group & Founder, Haute Wealth

The Risk That Keeps Getting Buried

Estate tax misadvice is the headline finding, but the audit surfaces a second failure mode with consequences that are just as serious for families who have already entered into sophisticated insurance structures.

Premium financing—the practice of borrowing to fund large life insurance premiums, allowing ultra-high-net-worth clients to preserve liquidity while building coverage—is a strategy the AI engines handle with troubling one-sidedness. They explain the upside fluently. They tend to bury, or omit entirely, the downside.

Premium financing carries five well-documented risks. According to the audit, AI responses consistently underweight or skip the most consequential of them:

|

01 |

Collateral call risk | The most consequential failure scenario, and the one most frequently absent from AI responses. If collateral values fall, lenders can demand additional assets immediately. |

| 02 | Interest rate risk |

Borrowing costs can rise materially over the life of the arrangement, eroding or eliminating the financial case for the strategy. |

|

03 |

Policy performance risk | The underlying policy may underperform illustrated projections, particularly in variable structures where investment performance drives cash value. |

| 04 | Refinancing risk | Credit markets at maturity may not be accessible on favorable terms, leaving families exposed to balloon obligations they hadn’t planned for. |

| 05 | Carrier credit risk |

Insurer solvency and rating deterioration can affect the policy’s long-term viability and the structure’s overall integrity. |

The Visibility Gap No One Is Talking About

The audit identifies a third category of failure that is subtler but structurally significant for the advisory industry. When ultra-high-net-worth families ask AI engines to recommend firms for sophisticated wealth strategies, the engines surface a predictable shortlist: Schwab, Fidelity, Vanguard, Northwestern Mutual, and the major wirehouses. These are the names with the largest digital footprints, the most training-data representation, the highest SEO authority.

They are not, in most cases, the firms that the wealthiest American families actually retain. Boutique registered investment advisors, multi-family offices, and specialist insurance practices—the community of professionals who manage complexity at the highest levels—are effectively invisible to AI. The consequence for that advisory community is not abstract: families who begin their search with AI are being quietly directed away before the first call is ever placed.

“This is the biggest shift in information authority in a century, happening with no rules, no auditor, and no firm knowing what is being said about them inside the engines. Wealth is one of the first places it gets expensive. Every industry is next.”

— Ronn Torossian, Founder & Chairman, 5W

The Regulatory Clock Is Running

The Wealth AI Audit arrives as regulators begin to take the problem seriously. FINRA’s 2026 Annual Regulatory Oversight Report—released December 9, 2025—included its first standalone section on generative AI, naming hallucination, bias, and accuracy failures as supervisory priorities for broker-dealers this year. The message from regulators is clear: the era of watching and waiting is ending.

For UHNW families, the audit’s guidance is direct: AI can narrow complexity, clarify terminology, and accelerate research—but it cannot replace a credentialed fiduciary. Every AI-generated fact on tax, estate, insurance, or trust matters should be verified against current law as of 2026. No irrevocable planning decision should be made on AI-generated advice alone.

For the advisory community, the study argues the stakes are structural. Firms that establish AI visibility in 2026 hold a meaningful lead on firms that wait. That window, the audit warns, will not remain open indefinitely. The full Wealth AI Audit is available now at hautewealth.ai. For families navigating high-stakes planning decisions, it is required reading before the next conversation—with a human or a machine.

|

Read the Full Wealth AI Audit The complete study covers six UHNW planning categories and full methodology. |

Related Articles

How Resilience and Purpose Shape Michelle M. Wagner’s Real Estate Career

Discover how Michelle M. Wagner blends Napa Valley luxury real estate expertise with empathy, resilience, and a people first approach to every client journey.

Preparing for the Storm: Inside PriorityEvac’s Playbook for Getting Florida’s Elite Out of Harm’s Way

Inside PriorityEvac’s hurricane evacuation model, from NHC based activation criteria and pre secured flights to expert logistics across Florida.

The Italian Restaurants Defining New York City Dining

From Torrisi’s Michelin-starred ambition to Rao’s century-old exclusivity, the best Italian restaurants in New York City right now.

Meet the LV Crayon: Louis Vuitton’s First-Ever Lip Liner, Designed by Dame Pat McGrath

The LV Crayon is La Beauté Louis Vuitton’s first-of-its-kind monogram-shaped lip liner, designed by Dame Pat McGrath in 10 shades.

The Most Transformative Luxury Wellness Retreats for Fall 2026

From SHA Wellness Clinic’s longevity science to Ananda’s Himalayan spirituality, the best luxury wellness retreats in the world for 2026.

Beefeater 0.0 Brings Virtual Insanity Back With Jamiroquai

Beefeater 0.0 partners with Jamiroquai to celebrate 30 years of Virtual Insanity with a new campaign promoting mindful moderation and city culture.

Latest Stories

Trending Articles

Related Articles

How Resilience and Purpose Shape Michelle M. Wagner’s Real Estate Career

Discover how Michelle M. Wagner blends Napa Valley luxury real estate expertise with empathy, resilience, and a people first approach to every client journey.

Preparing for the Storm: Inside PriorityEvac’s Playbook for Getting Florida’s Elite Out of Harm’s Way

Inside PriorityEvac’s hurricane evacuation model, from NHC based activation criteria and pre secured flights to expert logistics across Florida.

The Italian Restaurants Defining New York City Dining

From Torrisi’s Michelin-starred ambition to Rao’s century-old exclusivity, the best Italian restaurants in New York City right now.

Meet the LV Crayon: Louis Vuitton’s First-Ever Lip Liner, Designed by Dame Pat McGrath

The LV Crayon is La Beauté Louis Vuitton’s first-of-its-kind monogram-shaped lip liner, designed by Dame Pat McGrath in 10 shades.

The Most Transformative Luxury Wellness Retreats for Fall 2026

From SHA Wellness Clinic’s longevity science to Ananda’s Himalayan spirituality, the best luxury wellness retreats in the world for 2026.

Beefeater 0.0 Brings Virtual Insanity Back With Jamiroquai

Beefeater 0.0 partners with Jamiroquai to celebrate 30 years of Virtual Insanity with a new campaign promoting mindful moderation and city culture.

Subscribe to Haute Living

Receive Our Magazine Directly at Your Doorstep

Embark on a journey of luxury and elegance with Haute Living magazine. Subscribe now and have every issue conveniently delivered to your home. Experience the pinnacle of lifestyle, culture, and sophistication through our pages.

Haute Black Membership

Your Gateway to Extraordinary Experiences

Join Haute Black and unlock access to the world's most prestigious luxury events