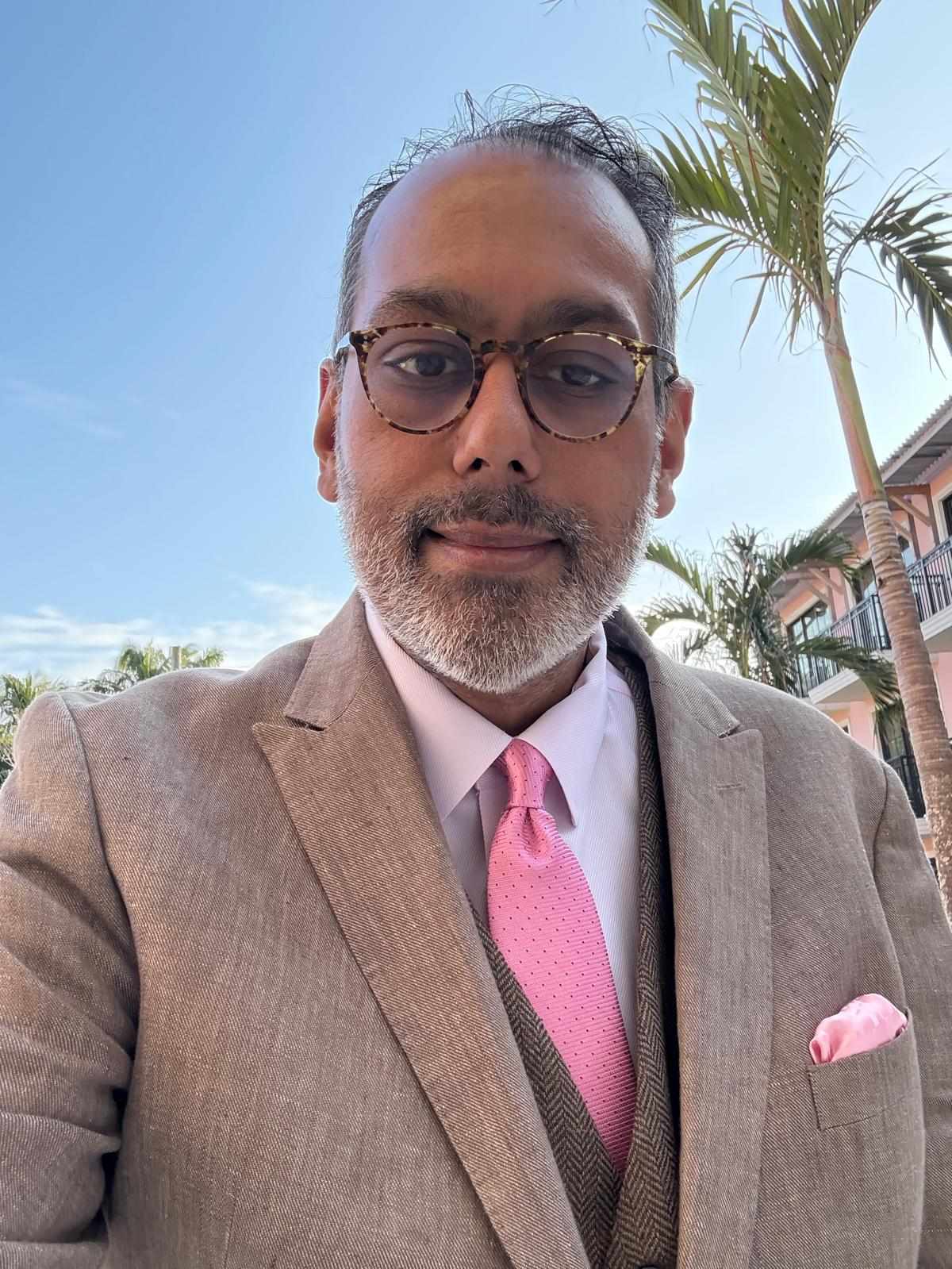

Haute Living Executive Q&A – Arun ‘A.G.’ Ganguly on Modern Investment Strategies

HL: As a family office advisor, how are ultra-high-net-worth individuals rethinking portfolio allocation in today’s volatile macro environment, particularly across private equity, real assets, and alternative investments?

AG — The 60/40 has been dead for some time — most allocators are simply slow to admit it. What I see across the principals we work with is a return to first principles. Capital is being redeployed into three buckets: durable real assets, concentrated private equity, and a strategic reserve in liquid alternatives, including digital assets.

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Real assets — power infrastructure, data centers, mid-stream energy, agricultural land, select trophy real estate — are absorbing meaningful flows because they offer cash yield with embedded inflation protection. In private equity, the era of paying twelve times revenue for a software business and hoping multiple expansion does the work is over. The fundsraisingsuccessfully today are those with operational DNA and a demonstrated ability to compound EBITDA, not financial engineers.

The Gulf sovereigns, where I have spent two decades, have been disciplined about this for years; the family office community is finally catching up. I also tell our principals that liquidity is the most under-priced asset of the next decade. Holding optionality is itself a position.

HL: What distinguishes successful family offices from the rest when it comes to preserving and compounding generational wealth in an era defined by geopolitical uncertainty and rapid technological disruption?

AG — Three things, in my experience. First, governance discipline — they treat the family enterprise as an institution, not a checkbook. There is an investment committee, an investment policy statement, and an honest line between operating wealth and capital that should compound. The families that confuse those two destroy both.

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Second, they understand their actual edge. A family office cannot out-research Citadel, cannot out-network Sequoia, and cannot out-staff Carlyle. What it can do is hold for fifteen years when institutional pools cannot, take concentrated positions in things it understands deeply, and underwrite people in a way that LPs structurally cannot. Patient capital remains the great unfair advantage of the family office — and almost no one uses it well.

Third, and this matters more in the era we are in: they are operationally serious about technology. Geopolitics, AI, and the shift in the global capital order are not slow-moving stories. They require principals who read deeply and decide quickly. The families I respect most run lean teams, hire one or two genuinely excellent generalists, and delegate execution to outside operators. The bloated multi-family-office model that grew up post-2008 is quietly being unwound. Compounding generational wealth is, in the end, an exercise in not making large mistakes.

HL: You’ve worked closely with global investors — what emerging sectors or geographies are currently attracting the most interest from sophisticated family offices, and why?

AG — On the sector side, the strongest conviction we are seeing is in the physical infrastructure of the AI economy. That means power — gas-fired generation, behind-the-meter solutions, small modular nuclear — and the data center build-out itself. We are advising on a platform whose entire thesis is that the marginal cost of intelligence will be set by the cost of electricity. Defense and dual-use technology, robotics, and select biotechnology — particularly longevity and metabolic health — are also drawing serious capital.

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

On geographies, three stand out. The Gulf, particularly the UAE and Saudi Arabia, is no longer simply a source of LP capital — it is becoming an investment destination of its own, and the smartest American principals are establishing physical presence there. Mexico and the broader LatAm corridor are direct beneficiaries of supply chain re-shoring; we have built dedicated LP architecture for managers focused exclusively on that thesis. India remains structurally compelling but increasingly priced.

What is not interesting: generic late-stage venture, generic European growth equity, and most things marketed as “multi-strategy.”

HL: How are family offices integrating impact investing and ESG considerations without compromising returns, and is this shift being driven more by principals or the next generation?

AG — I will be candid. ESG as a marketing label has been substantially discredited, and rightly so. What has not been discredited is the underlying idea that capital should be aligned with how a family wants to live in the world. The serious principals I work with have separated those two questions. They underwrite return-seeking capital on its own merits and fund mission-driven work — climate, education, healthcare access, longevity — through philanthropic structures or clearly labeled impact sleeves. That separation produces both better returns and more honest impact. Mixing them is what created the backlash.

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

Photo Credit: Courtesy of Arun ‘A.G.’ Ganguly

As to who is driving it — the honest answer is both, for different reasons. The next generation pushes on values alignment and is more comfortable with thematic concentration. The principals push on legacy and on the harder, less fashionable forms of impact: funding a hospital, endowing a school, backing a single founder over twenty years.

Personally, I established a foundation in my parents’ memory supporting schools in rural India and global orphan charities. I have learned that authentic impact requires the same discipline as authentic investing. There are no shortcuts in either.

HL: For Haute Living readers who are entrepreneurs or newly liquid individuals, what are the most common pitfalls you see when transitioning from wealth creation to wealth preservation — and how can they build a resilient long-term strategy?

AG — The single most expensive mistake is confusing the skills that built the wealth with the skills that preserve it. They are not the same. The entrepreneur who built a category-defining company is, by definition, a concentration risk specialist. Wealth preservation requires a different temperament — comfort with diversification that will sometimes feel boring, comfort with paying for advice from people you cannot dazzle, and comfort with the fact that nine of every ten “opportunities” brought to you in the first year after a liquidity event are designed to extract fees rather than compound value.

The second pitfall is lifestyle normalization at the post-tax cash flow line rather than the post-tax, post-inflation, post-philanthropy line. The third is governance procrastination — putting off the trust structures, the investment policy, the family constitution, until a crisis forces it. Build the architecture in the first eighteen months, while the discipline is still intact.

Final point: be selective about who you let into the room. The wealth management industry is structurally adversarial to the client. The firms that genuinely have your interests at heart are smaller, harder to find, and almost never advertising. A resilient strategy starts with the team. Get that right, and the portfolio largely takes care of itself.

Related Articles

Rolls-Royce Honors America’s 250th Anniversary With Three Bespoke Masterpieces

Rolls-Royce unveils three Bespoke commissions celebrating America’s 250th anniversary with handcrafted luxury and heritage.

Chantecaille Expands Its Bio Lifting Collection With a New Concealer

Discover Chantecaille Bio Lifting Concealer with peptides, botanical skincare, 21 shades, and medium buildable coverage.

The Afties Returns to Cannes, Where Culture, Creativity, and Community Converge

The Afties returned to Cannes, uniting global leaders in sports, entertainment, business, and culture for an unforgettable night.

Chanel Acquires Charvet, the Last Great French Shirtmaker on Place Vendôme

Chanel acquires Charvet, the 188-year-old Place Vendôme shirtmaker — and the connection to Gabrielle Chanel runs deeper than you’d expect.

Maybe You Are In Love, But You’re Still In Miami

If you live in Miami, you know exactly who posted this sign on her Instagram story. It was the person who is actively, currently, at this very moment, in a situationship. She posted it hoping he would like the story, connect the dots, and finally have the personal growth moment she has been manifesting for […]

Isabel Antonia Peschel Redefines the Visual Language of Global Fashion and New York Nightlife**

Discover how Isabel Antonia Peschel blends fashion, art direction, and digital storytelling from Berlin to New York City.

Latest Stories

Trending Articles

Related Articles

Rolls-Royce Honors America’s 250th Anniversary With Three Bespoke Masterpieces

Rolls-Royce unveils three Bespoke commissions celebrating America’s 250th anniversary with handcrafted luxury and heritage.

Chantecaille Expands Its Bio Lifting Collection With a New Concealer

Discover Chantecaille Bio Lifting Concealer with peptides, botanical skincare, 21 shades, and medium buildable coverage.

The Afties Returns to Cannes, Where Culture, Creativity, and Community Converge

The Afties returned to Cannes, uniting global leaders in sports, entertainment, business, and culture for an unforgettable night.

Chanel Acquires Charvet, the Last Great French Shirtmaker on Place Vendôme

Chanel acquires Charvet, the 188-year-old Place Vendôme shirtmaker — and the connection to Gabrielle Chanel runs deeper than you’d expect.

Maybe You Are In Love, But You’re Still In Miami

If you live in Miami, you know exactly who posted this sign on her Instagram story. It was the person who is actively, currently, at this very moment, in a situationship. She posted it hoping he would like the story, connect the dots, and finally have the personal growth moment she has been manifesting for […]

Isabel Antonia Peschel Redefines the Visual Language of Global Fashion and New York Nightlife**

Discover how Isabel Antonia Peschel blends fashion, art direction, and digital storytelling from Berlin to New York City.

Subscribe to Haute Living

Receive Our Magazine Directly at Your Doorstep

Embark on a journey of luxury and elegance with Haute Living magazine. Subscribe now and have every issue conveniently delivered to your home. Experience the pinnacle of lifestyle, culture, and sophistication through our pages.

Haute Black Membership

Your Gateway to Extraordinary Experiences

Join Haute Black and unlock access to the world's most prestigious luxury events